Single-Point Adjustments in Deltek Cobra

Single-Point Adjustments in Deltek Cobra

The term Single-Point Adjustments (SPA or S&P=A or S=P) is an oft used process on Cost-Plus type projects. Its purpose is to essentially erase cost and/or schedule variances to date and replan the remaining effort consistent with the remaining scope of work. Further, the remaining effort is planned with the remaining negotiated cost and any Authorized Unpriced Work (AUW), if applicable.

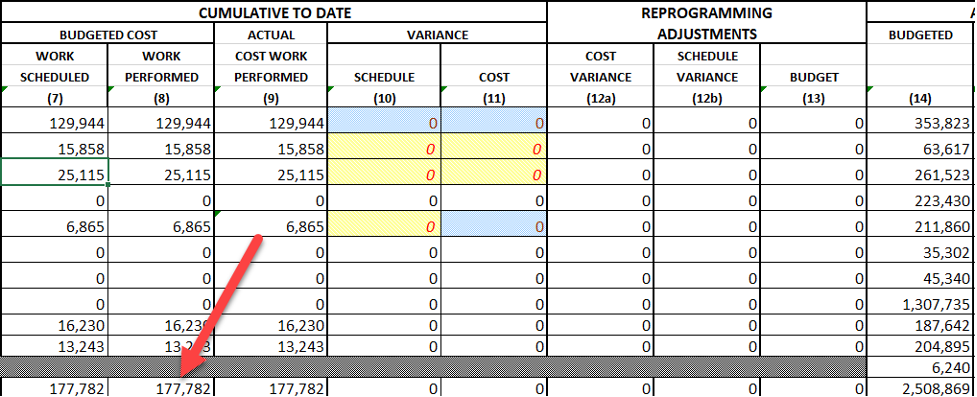

This operation typically sets BCWS (budgeted effort) and BCWP (Earned Value) equal to the ACWP (Actual costs) as of a certain period end date. Alternatively, the operation may only address the schedule variance, where BCWS is set equal to BCWP. This blog will focus on erasing both the cost and schedule variances (S&P = A).

The justification often used for the Single-Point Adjustment, or Replan (will use this term for the remainder of this blog) is that the current baseline is so far out of touch with reality that it no longer provides accurate or meaningful performance data. This could occur due to significant design changes, schedule delays whose causes are independent of the contractor’s control, or most often, the distaste many have of having to look at poor performance that just won’t go away.

Usually, when a Replan is appropriate to a project (which it often isn’t), the causes of past variances are in the past and further significant variance growth is not anticipated. In other words, what happened in the past is not expected to continue and now a realistic plan can be developed.

An argument for the Single-Point Adjustment

It does occur at times where the execution of a project varies significantly with how the effort was originally planned in the baseline. Determining progress becomes difficult when the activities in the current plan differ from the tasks that are now being performed, as well as who is now performing them. As a result, confidence that the progress earned is truly representative of overall project status is low.

Additionally, difficulties early on in a project, such as design challenges that required significant re-design effort, may have incurred significant cost overruns that are not anticipated to continue. It can be assumed that this rework may have significantly affected how the remaining effort will be executed, therefore justifying updating the baseline accordingly.

An argument against the Single-Point Adjustment

As noted above in paragraph 2, it was suggested that the Replan process is often employed where it is not necessarily helpful. The experience of the Cobra Guy affirms that, more often than not, the Replan process is employed to erase cost and schedule variances, which are ugly and unpleasant to look upon.

The scope of work hasn’t changed, the execution approach remains the same and the allocated budget at the project level is unchanged. I have also determined that usually the Replan is only employed when variances are unfavorable.

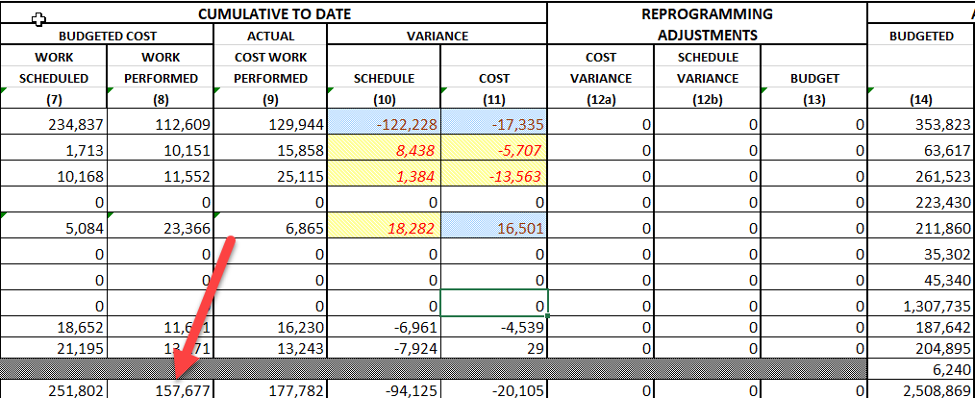

The challenge in this scenario is that the negotiated cost has not changed, thus the remaining dollars to be replanned are reduced from what was in the original baseline. Assuming the cost variance is unfavorable and that the BCWP will be set to equal the ACWP, the remaining budget $ will be reduced by the amount of the unfavorable cost variance.

Said another way, where there is an unfavorable cost variance. In other words, the BCWP is less than the ACWP, the BCWP increases by the amount of the unfavorable cost variance.

Herein lies the rub. The value for the work completed just went up, while the amount of effort actually completed remains the same. This reduces the total budget $ remaining.

The issue is, that this process assumes the project team can execute the remaining work for less money than previously. Yet the justification for the Replan exercise was an unfavorable cost variance. Most would agree that past poor cost performance does not lead to future great cost performance.

A common method of validating whether a project can complete the remaining effort on budget is to compare the “To Complete Performance Index” (TCPI) – where the required efficiency to achieve the budget is calculated – to the Cost Performance Index – the efficiency achieved to date. Where there is a significant delta between the two metrics, it is understood the chances of achieving the required performance level is deemed practically nil. Thus, it can be assumed that the situation which led to the Replan will repeat itself, thus nullifying the intent of the Replan itself.

So, what to do?

I see no value in erasing cost and schedule variances where the execution plan has not significantly changed. Variances are to be expected on development projects, thus the Cost-Plus contract type, which acknowledges the risks and uncertainties encountered in these projects. The attitude toward variances should be one of inevitability – something to be managed and understood – not to be buried.

The following steps can be employed to meaningfully address cost and schedule issues, while maintaining variances to the plan.

- Provide meaningful variance analysis. Identify the root cause. What had been planned and what happened instead. For cost variances, both identify the underlying cause and then explain how it resulted in a variance. Rework required? Higher paid resources than planned? Vendor price changes? This of course requires the Control Account Manager to know what is in the baseline, which brings us to the next step:

- Schedule a weekly look-ahead. This meeting reviews current and upcoming tasks, the accuracy of the dates and applicability of the resources planned to execute the effort. This is one of the most effective methods of identifying cost and schedule issues before any work begins.

Compare this to the more common approach of executing the work, never referring to the budget for the task and dealing with the variances once they are reported. This should be an obvious approach to identifying variances before they’re incurred. Often, the data relevant to performing the weekly look-ahead is posted on a server instead of actually holding the meeting. This will not accomplish its purpose, as the CAMs do not review the data. Sorry CAMs, but that’s the truth.

- Develop a realistic Estimate to Complete (ETC). Once a project has a few months under its’ belt, the task of estimating remaining work begins. There are many tools for performing this task (another blog topic), but ultimately the project team will be executing to the ETC, not to the budget. Yes, I know this is a controversial subject, but once both the contractor and the customer agree on the validity of the ETC, this becomes the plan. While variances are still calculated against the current budget, it is the ETC that drives the effort.

While variances are certainly to be expected on development projects, CAMs still need to be held accountable. The variance analysis report includes a section for the correction action employed. These should become action items to be tracked. The CAMs are indicating something they plan to employ to mitigate the impact of the variance.

These should be re-visited during the next Program Management Review to assure the corrective action was, in fact, executed. If not, why?

It should be acknowledged that poor planning and scheduling of resources which result in cost and schedule variances becomes a personnel issue, not an inevitable project execution issue, requiring PM action to rectify.

Now that the Cobra Guy has done all he can to dissuade use of the Replan process, it still can be useful and appropriate in certain cases. The steps and options in executing the process will be addressed in an upcoming blog.