An important decision to be made during the earned value system setup process is how best to load actual costs into Deltek Cobra. There are two basic options: a cumulative load and a current period load. The choice that will work best for your system depends on many things. You must know how Deltek Cobra behaves in each case in order to make the right decision.

In this article, we give you the facts and examples that show how Deltek Cobra will process the two types of actual cost records. Once you have the facts, you can make a better decision on which type loading method will work best with your system. To save you some time, we’ve run a couple of tests and show you the results using screen shots. This way you get to see firsthand what Cobra does in each case.

Overview

Cumulative Actual Costs

Using the cumulative actual costs option means that you provide Cobra with a CSV file containing actual costs that run from project inception to date. These actuals must be grouped and summarized, typically by work package and then by resource. Cobra will load the latest cost amount for each work package or control account (depending on your setup) and then compare that to the total for the prior period. The delta is the current period cost you see in your CPR format reports.

Pros and Cons

Pro – The cumulative actual cost method is self-correcting. If changes are made to prior period costs in the finance system, no additional processes need to be performed to accrue these changes in Cobra.

Con – The cumulative actual cost files require more processing up front to get the data into a proper state for Cobra importing. This processing can usually be automated using scripts or simple programs within the finance system.

Current Period Actual Costs

Using the current period actual costs option means Deltek Cobra will process the amounts into the current period with the assumption that these costs represent only values collected for the current reporting period. It will add these values to previously loaded actual costs to generate the cumulative costs.

Pros and Cons

Pro – The current period actual costs do not need much preprocessing to build the CSV source file, so little or no scripting or programming is required in the finance system.

Con – The current period actual costs are not self-correcting. Changes made in the finance system will need to be loaded using a separate process to accrue the correct totals.

We’ve run a couple of tests to demonstrate the differences in loading actual costs using these two options.

Actual Cost Data

Cumulative Actual Costs

The examples below show simple cumulative cost files ready for import into Deltek Cobra. You can see how the hours accumulate over each period. The data has been summarized to show every hour worked by each person on a particular work package since the project’s inception to the end of the current period.

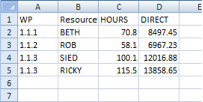

Month 1

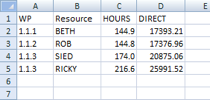

Month 2

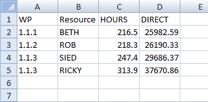

Month 3

We’ve loaded all three of these into Cobra and here are the results.

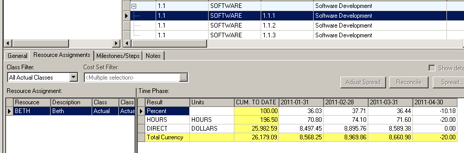

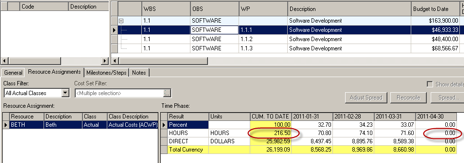

In looking at the three periods loaded, you can see how Cobra has calculated the current period values by saving the delta for each cumulative value it read into each period. The major benefit to this method is its ability to automatically correct values when changes are made in the accounting system.

For example, if finance moves money around in prior periods already loaded into Cobra, the total loaded in the current period may go down or up. For example, if Beth had booked 20 hours to the wrong task in a prior period, and finance caught the error and moved the hours off 1.1.1 for Beth, the total posted in the current month would be 20 fewer hours for work package 1.1.1. When the cumulative total is loaded for the current month, it will have gone down by 20 hours, automatically correcting the cumulative total for that work package. This is what is known as an “adjusting entry”. If no other hours are booked by Beth to that work package after the change, the cumulative total will have dropped from 216.5 hours to 196.5. We’ll show that in the 4th reporting period of our example in Cobra.

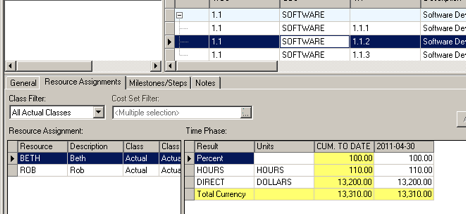

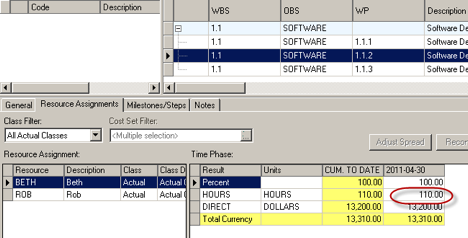

This is the file for period 4. Beth’s hours dropped by 20 on 1.1.1 and were moved to 1.1.2. Beth also booked another 70 hours to 1.1.2 increasing this period’s total to 110 hours.

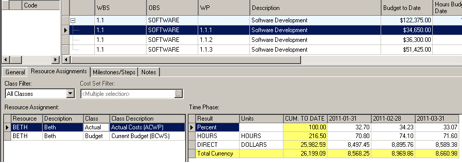

After performing the load of period 4, you can see that the period correctly shows -20 hours for work package 1.1.1.

And in the above figure, you can also see the total of 110 hours for work package 1.1.2. An adjustment made in period 3 has shown up as an adjusting entry in period 4. Because you can never change history in an EVM system, this is the legitimate way to correct mistakes, and the correction happens automatically when using cumulative actual cost methods.

Current Period Actual Costs

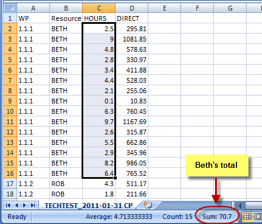

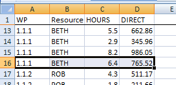

Current period actual costs do not need to be summarized in the same way that cumulative actual costs do. In the example below you can see that these values originated in a timesheet system, so the values are daily. Cobra will read in each record and summarize the data against the respective work packages, and resource as it goes.

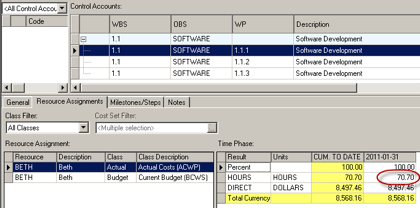

Note Beth’s total of 70.7 hours. The next figure shows how Cobra correctly read in and totaled each record for Beth when the data was loaded as current period values.

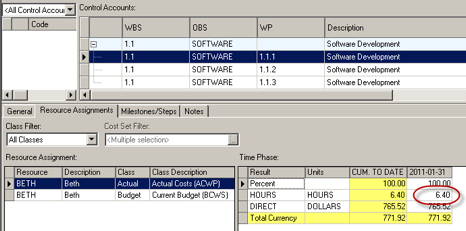

For demonstration purposes, it’s helpful to demonstrate what would happen if we made a mistake and tried to load a current period formatted CSV file as cumulative.

In the above example, we loaded the same current period CSV file as in the previous example, except we deliberately used the Cumulative option. What happened? Why did only 6.4 hours get loaded?

When you look at the content of the CSV file, you can see exactly what happened. Cobra read in each record, but immediately replaced it with the next record, then replaced that with the next record, and so on. It didn’t summarize the rows because it was expecting a single summarized record for Beth, working on WP 1.1.1. So we ended up with only the hours recorded in the last 1.1.1 record for Beth, in this case 6.4 hours.

In the cumulative actual costs test, we showed you how changes are self-correcting when they occur in the financial system. With current period actual cost loading, however, you would not know that finance corrected some prior period hours. If finance moved 20 hours of Beth’s work to 1.1.2 and she didn’t book anything further to 1.1.1, you wouldn’t even see a record in the current period file. Beth has simply dropped off the 1.1.1 work package. The current period costs file would look like this.

In the example above, you can see Beth’s new total of 110 hours for period 4 on 1.1.2, but the 20 hours that were moved in period 3 are not accounted for because we only pulled current period actual costs from the finance system.

If we load this, our current period costs will be 20 hours more than they should be for 1.1.1 because there’s no adjusting entry. Here’s what happens.

You can see the 110 hours for Beth on the 1.1.2 work package. So far, so good.

But what about the 20 hours that were moved in period 3?

Here’s the problem. Work package 1.1.1 still shows the total hours for Beth to be 216.5; no adjusting entry has made the necessary correction. Therefore, the cumulative total hours appears to be 326.5. The actual total, however, if one checks with the finance system, is 306.5. The net result of this error is an administrative cost variance of $2,400.

The real problem is you won’t even know this unless you have good habits and regularly check the Deltek Cobra cumulative actuals total against the finance systems numbers – a habit you will most definitely need to adopt if you’re planning to run your system with current period actual cost loading. Unless the additional bogus hours build up within the control account to such a degree that they exceed a threshold, Cobra has no way to let you know there’s a problem. This isn’t a shortcoming on Deltek Cobra’s part, it’s just the simple fact the Cobra can only work with what it knows about the actual costs; current period loading puts the onus on you to keep an eye on the cumulative figures.

The solution is to check the cumulative totals periodically against the finance system, create actual cost files that contain all the required adjusting entries, and run that in as a separate process. This can get complicated and the longer you wait, the harder it gets. Accepted industry practice is to run these adjusting entries quarterly, but this may vary, depending on your customers’ or your company’s comfort level.

This should give you a good starting point when considering whether to use cumulative or current period actual cost loading methods. There are pros and cons to each method, but both do require some work. It’s a matter of when you want to do that work. Cumulative actual cost loading may require some additional time on the front end, depending on how much effort it takes to get cumulative actual cost summary spreadsheets out of your financial system, while current period actual cost loading requires more time later, to run the adjusting entries.