Everyone recognizes that Management Reserve (MR) is a key component of good project management, but it is often misunderstood and ill-defined. In this article by Mark Infanti, EVM Subject Matter Expert, MR is explained in a way that helps the reader understand where MR fits into the overall project structure and how it is different than funding contingency.

MR is defined in EIA 748 Earned Value Management Systems, the commercial standard for EVMS, as “An amount of the total budget withheld for management control purposes, rather than being designated for the accomplishment of a specific task or set of tasks.” In most programs, particularly developmental efforts, there is considerable uncertainty regarding timing and/or magnitude of future difficulties such as:

- Growth within currently authorized work scope

- Rate changes (overhead, labor, material, currency, etc.)

- Risk – its probability of occurrence and its impact

- Other program unknowns

Consequently, MR is established to provide a source of budget to plan and execute effort initially excluded from the project plan, which is necessary to overcome these difficulties and keep the project on track.

Many people incorrectly view MR as funding contingency. In order to better understand MR, the difference between funding and budget must be well understood. Budget is the estimated cost for the planned work agreed to by both contractor and customer. Funding is the amount of money held by the customer to reimburse the contractor’s actual costs and fees or price (depending on the contract type).

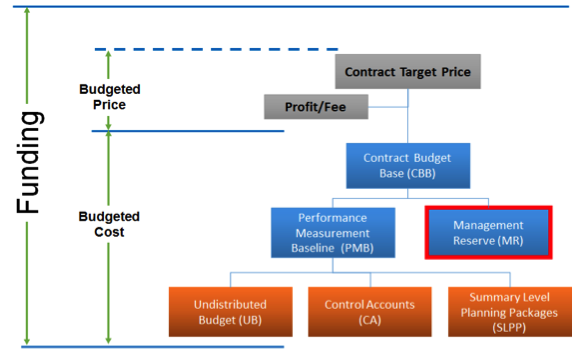

Figure 1 illustrates the classic relationship between budget elements and funding.

Figure 1 Budget/Funding Relationship

Figure 1 Budget/Funding Relationship

A customer generally requires funds in excess of the contractor’s budget to pay for contract changes and overruns (if allowed by the contract). OMB encourages customers (federal agencies) to establish Program Risk-adjusted Budgets (PRB) to provide funding and schedule contingencies to cover the risk of cost and schedule overruns on a project.

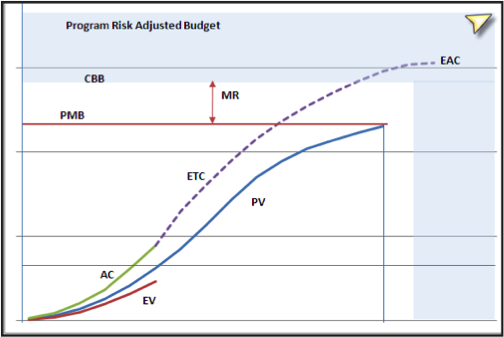

Figure 2 shows how the MR, which is part of the contractor’s budget, relates to the customer’s contingencies comprising the program risk adjusted budget.

Figure 2 – Budget and Funding Profiles

In this diagram you can see the difference between the contractor’s CBB and the customer’s Program Risk Adjusted Budget (PRB), depicted by the shaded area. The PRB includes the amount of additional funds and time that the customer has available to handle cost and schedule growth that may occur on the project. As the name implies, it is based on the risks identified by the customer for the project, which are usually based upon the customer’s history and experience with similar projects. The horizontal scale, representing time, shows that the PRB is planned to a date beyond the contract end date. This is the equivalent of schedule contingency or reserve that may be held by the customer.

The blue line is the total time phased budget or planned value (PV). The total of the entire planned budget is the Budget at Completion (BAC). Above that, is the contractor’s Management Reserve (MR). The BAC + MR = the Contract Budget Base (CBB). This is the total estimated ‘cost’ of the project.

Above that is fee, which when added to the CBB yields the Contract Target Price (CTP), (not shown).

Upon completion of a contract, some MR often remains. This may be true whether the contractor’s final actual cost was over or under the contractor’s planned cost at completion or BAC. Many people find this bothersome due to their confusion over the differences between budget and funds.

Ultimately, the contractor will be paid, from funding allocated to the contract, for all contractually allowable costs and fee incurred in performance of the project. This may end up being in excess of the budget (overrun) or less than the budget (under-run) and any remaining MR is simply a number in a log.

Read the second article in this three part series Estimating Management Reserve (MR)