There is a lot of confusion about some of the terminology surrounding the process of Earned Value Management (EVM). This can be particularly confusing for those who are new the discipline of Earned Value Management. There are various monetary terms that, while probably somewhat familiar to you, will not always make immediate sense when used in the context of EVM.

There is a lot of confusion about some of the terminology surrounding the process of Earned Value Management (EVM). This can be particularly confusing for those who are new the discipline of Earned Value Management. There are various monetary terms that, while probably somewhat familiar to you, will not always make immediate sense when used in the context of EVM.

Earned Value Management Terminology

This article takes a high-level look at earned value management terminology and attempts to put it into context.

Budget

Financial Definition: A statement of the financial position of an administration, for a definite period of time based upon estimates of expenditure during the period and proposals for financing them.

Project Management Definition: A plan for the coordination of resources and expenditures.

The term budget means different things to different people, depending on their role. To a corporate manager, it means the amount of money his department has been allocated to run on for some specified period. To a homemaker, it means the income that the household has to live on every month. To a project manager it will be a contract value: an amount that will be distributed out over a time-phased plan of work.

In earned value the term ‘budget’ is used as a general terms for hours, dollars, materials, equipment and other finite resources available to complete a given project. For the purposes of earned value a better term comes from the PMI camp: namely “Planned Value”. The reason this terminology is more accurate for earned value is based in the fact that, contrary to popular misconception, earned value is a performance measurement function, not an accounting function. Budget is generally considered an accounting term. Planned value, on the other hand is descriptive of a plan to earn specific amounts of value over a specific period of time.

We will earn value based upon that plan when we start to perform that work, and hopefully we will do so as closely to that plan as possible. If not, we will not earn the necessary value, and thus show a shortfall in progress. This shortfall will be expressed in terms of schedule variance and cost variance.

Undistributed Budget (UB)

This is any amount of the contract’s planned value that has not been allocated to work packages, control accounts, or planning packages in the project. Long term balances in the UB account is not a good thing because it highlights that we have failed to allocate time and resources fully to our intended plan. You can think of UB as orphan dollars that need a home. The DCMA and other overseeing groups frown on UB and expect you to distribute the unallocated resources within 60 days of project start.

Distributed Budget (DB)

This term refers to all the allocated planned value resources in the project. It is the total cost of all work planned for the entire project.

Management Reserve (MR)

Management Reserve is one of the most misunderstood categories of project finance in the industry. Some less informed entities think it’s some kind of slush fund to finance back door changes or other nefarious off-book dealings. Poppycock: it’s nothing of the sort.

Management Reserve is a necessary and important risk management tool. No project will ever go exactly to plan, ever – that is an inescapable fact. Ignoring this fact is foolish. Planning for the unexpected is wise. Management reserve is a dollar amount that is put by for ‘in scope but unplanned expenses’. The process typically includes a risk register that is used to define and quantify project risks. These can be anything: bad weather, late deliveries, environmental saboteurs, you name it. The risk register allows the project manager to understand the potential cost of these risks and put that amount aside as MR for use if any of the risks become a reality.

Fee

This is simply the amount that the company expects to make in profit after completing the project.

Control Account (CA)

Defined at the point where the Work Breakdown Structure (WBS) meets the Organizational Breakdown Structure (OBS): a control account represents a defined work scope given to a single organizational unit (and single manager) responsible for work performance. This person is usually the department head for the responsible organization (not performing organization as these could be many) and is known as a control account manager or CAM. In short, a control account is an object that represents a summary of all work required to deliver a particular item in the work breakdown structure.

Work Package (WP)

Work packages are natural subdivisions of control accounts. A work package is simply a task or set of tasks that describes the work required to complete a deliverable. A work package is the point at which work is planned, progress is measured, and earned value is calculated. Control accounts contain one of more work packages.

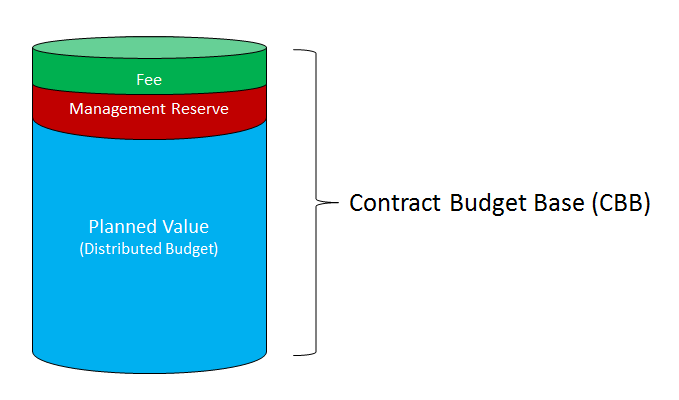

Contract Budget Base

The distributed budget, the management reserve and the fee should all add up to the Contract Budget Base. This will be the negotiated cost for the entire project. If it is a Firm Fixed Price contract this will be the ‘not to exceed’ amount. More commonly however, earned value is required on cost plus percentage of cost contracts as the customer is assuming more risk and will require strict accounting of expenses of the contractor.

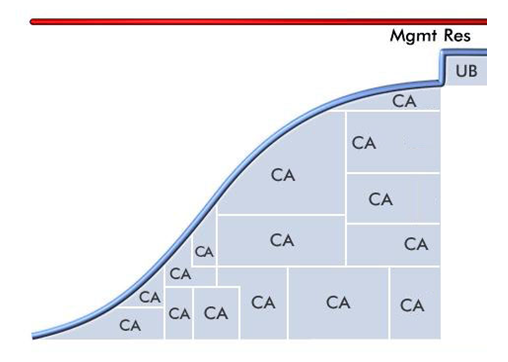

Another way to look at these elements is to see it in more of a time-phased way using this classic EVM diagram. The control accounts (CA) show the buildup of cumulative costs over time, any undistributed amount that may be present, and a risk mitigation allowance in the form of management reserve. This diagram ignores the fee aspect of the project’s contract cost model but does show the all-important time-phased aspect of an EVMS budget.

Another way to look at these elements is to see it in more of a time-phased way using this classic EVM diagram. The control accounts (CA) show the buildup of cumulative costs over time, any undistributed amount that may be present, and a risk mitigation allowance in the form of management reserve. This diagram ignores the fee aspect of the project’s contract cost model but does show the all-important time-phased aspect of an EVMS budget.

Most leading earned value management software systems have ways to account for these various earned value financials and help you correctly track the movement of such amounts between the accounts as changes are made to the contract.

Most leading earned value management software systems have ways to account for these various earned value financials and help you correctly track the movement of such amounts between the accounts as changes are made to the contract.

Summary

Earned value financial terminology can be a little confusing to people who are new to the discipline. With particular attention to the term budget, we suggest you always think of budget as planned value: i.e. a plan of how we intend to earned value on this project.

If all goes well, we will make progress more or less in the way we planned, giving us good earned value numbers.

We also hope to collect actual costs very close to the planned value in order to keep all our EV metrics looking good. The more we deviate from the planned value the worse our metrics look. Understanding this basic concept is key to good interpretation of the earned value reports.