The Responsibility Assignment Matrix, or RAM, is one of the fundamental charts or matrices used on an ANSI/EIA-748 project. It articulates the translational point from where detail cost, schedule and technical performance data is summed from and reported to internal and Government agencies.

Additionally, this is the point at which Control Account Managers (CAMs) are assigned the Responsibility, Accountability and Authority (RAA) to develop detail plans. These plans include provisions for the scope, schedule, resource allocations needed to perform the work. They also include technical performance assessments and analyze any associated risks, coupled with their mitigation, for those segments of work assigned to them in their respective Control Account (CA).

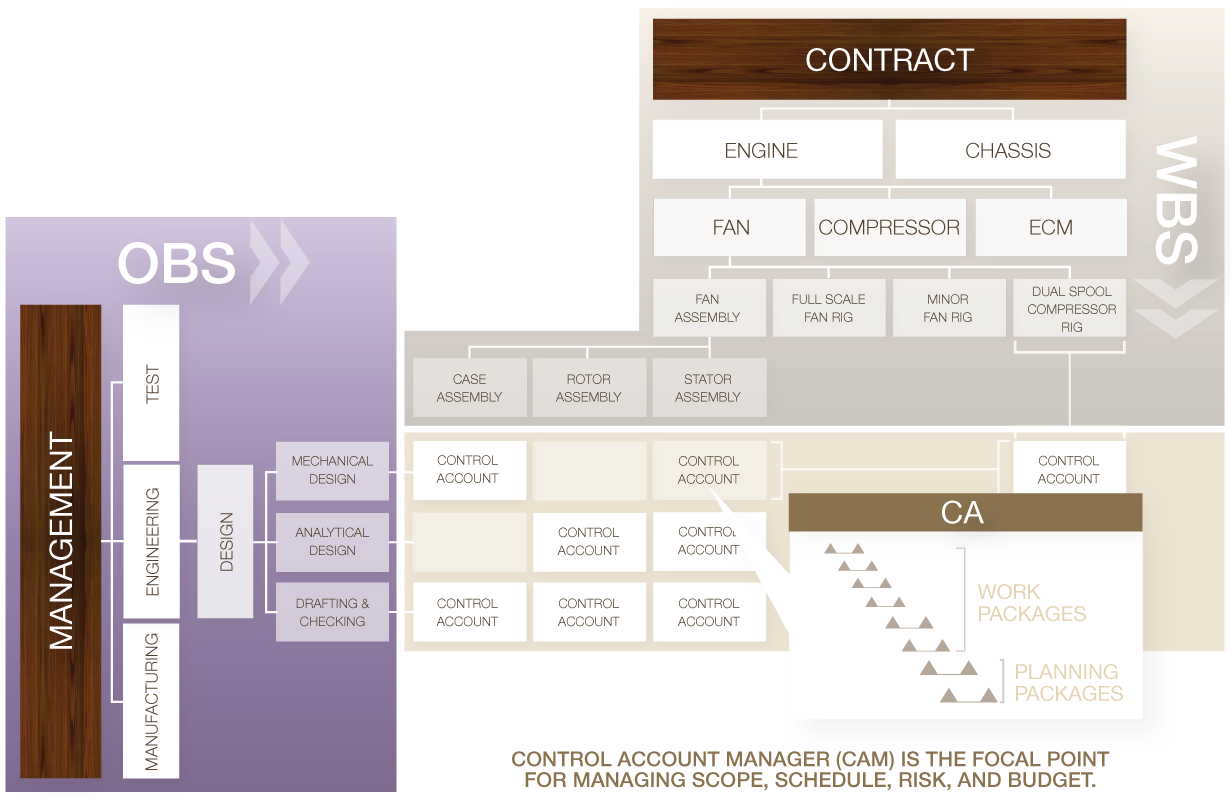

The figure below illustrates the segmentation of work from the top-level Contractual summary down to the portions assigned to the respective CAMs.

Each CAM is responsible for the planning, execution, technical performance assessment, cost comparison and risk analysis/mitigation for their assigned segments or Control Accounts (CA). Periodically, each CAM must summarize the cost, schedule, technical performance and risk analyses in order to determine any cost and/or schedule variances from the current plans. I addition, they will need to determine any necessary recovery mitigations required and to assess any impacts on theirs and other CAs cost and schedule performance.

The Responsibility Assignment Matrix is a critical element in the process of determining if RAA has been assigned in a manner that will effectively facilitate the contractual performance of scope, schedule and technical requirements. This is accomplished by doing a number of summaries for the Total Contract and for each CAM. This allows both internal and external management to be reasonably assured that each CAM has not been assigned more RAA than can be reasonably be expected to effectively execute. These summaries are listed below:

- Total Hours/$/% broken down by Labor, Material, Subcontract, Other Direct Costs (ODC)

- To better understand the composition of elements of cost within a CA

- Total Hours/$/% broken down by Total Discrete, Apportioned, Level of Effort and Planning Packages

- To better understand how the CA’s effort is being detail planned and how much if any is distributed to the future in Planning Packages (PPs)

- Total Hours/$/% for all Discrete broken down by Earned Value Technique being used

- 50/50, 0/100, Milestones with % complete, Subjective % Complete, other

- To get a better understanding as to the basis of the fidelity of the percent complete that the CAM will be reporting as their performance progress metrics

- 50/50, 0/100, Milestones with % complete, Subjective % Complete, other

- At the total Contract level a summary will normally be expected to show Hours/$/% for each of the following:

-

- Distributed Budget

- Undistributed Budget

- Management Reserve

- Total Budget

The purpose of the latter is to demonstrate how well the project has been authorized, detail planned to date and will be substantiated by data contained in the CAMs detail RAMs.

Additional summaries may be necessary if, for example, a project is in process and both internal/external management desire to see how much effort has been completed to date.

Summary

The Responsibility Assignment Matrix is a tool used by internal and external management. It’s used to understand the magnitude of effort contained in a Contract and how it has been distributed to the CAMs, who have the ultimate RAA to execute them on behalf of the Program Manager.

This is a critical tool that will always be used in Integrated Baseline Reviews (IBRs) by the Customer to ensure that all Contractual work can be reasonably expected to be performed. This is based on cost, within schedule, meeting technical requirements and successfully producing Contractual Deliverables as defined in the Contract’s SOW.